This is an important section that Indians must be aware of before making their move to Spain. It is important to understand the equation of taxes on both sides.

If you spend more than 183 days in Spain in a calendar year and you are a Spanish tax resident for that year. Days do not need to be consecutive. Once you cross this threshold, Spain taxes you on your worldwide income, your Indian salary, rental income from Indian property, dividends from Indian stocks, interest on fixed deposits, and every other global income source.

Even if you spend fewer than 183 days in Spain, you can still be considered a Spanish tax resident if your main economic interests are based in Spain. For example, if your primary business or investments are there. The 183-day rule is the most common trigger, but it is not the only one.

Spain follows a calendar-year tax system (January to December), unlike India’s financial year (April to March). This difference can create split-year tax complexities in your year of relocation, making professional tax advice especially valuable during your first year.

Spain's Beckham Law is a special tax regime that allows qualifying new residents to pay a flat 24% tax rate on Spanish-sourced income up to €600,000 for their first six years in Spain, instead of the standard progressive rates which rise up to 47%. For income above €600,000, the rate is 47%.

For Indian professionals earning above €30,000 annually in Spain, which covers most IT professionals, consultants, and finance workers. The Beckham Law is a financial advantage. The difference between paying 24% flat versus progressive rates up to 47% compounds meaningfully over six years.

Who Qualifies?

To qualify for the Beckham Law you must:

The 6-month application window is strict and non-negotiable. You lose the benefit for all years if you miss this window. The moment you register with Social Security after arrival, put the Beckham Law application deadline in your calendar immediately.

Does It Apply to DNV Holders?

Yes, Digital Nomad Visa holders can qualify for the Beckham Law provided they meet the conditions above. The 2023 Startup Act that created the DNV extended Beckham Law eligibility to remote workers and digital nomads, which was an important change from the previous rules.

How to Apply

The application is filed with the Spanish Tax Agency using Modelo 149. Given the financial stakes, this is one process where engaging a Spanish tax advisor with expatriate experience is strongly recommended rather than attempting it independently.

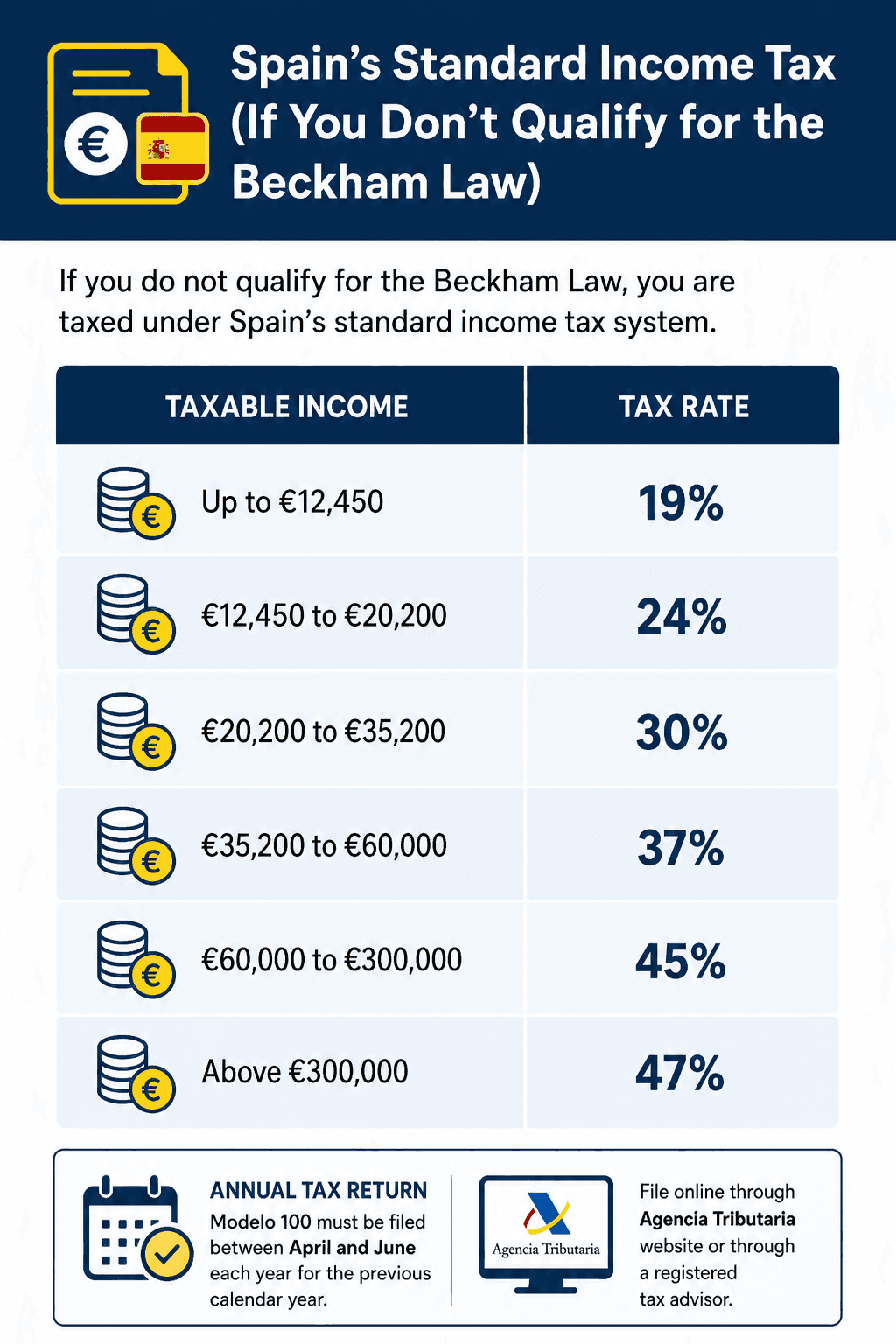

If you do not qualify for the Beckham Law then you are taxed under Spain's standard income tax system.

Your annual tax return- Modelo 100 must be filed between April and June each year for the previous calendar year. Filing is done through the Agencia Tributaria website or through a registered tax advisor.

Modelo 720 is Spain's foreign assets declaration. Any Spanish tax resident who holds assets outside Spain above certain thresholds must declare them to the Agencia Tributaria by 31 March of the year following their first year of Spanish tax residency.

The three categories are:

You only need to file Modelo 720 once for each category and then refile only if the declared value increases by more than €20,000. The declaration is informational, it does not create an additional tax liability on its own but failure to file when required is a serious compliance breach. If you have Indian property, meaningful savings, a mutual fund portfolio, or a PPF or NPS account, Modelo 720 applies to you.

India and Spain have a Double Taxation Avoidance Agreement (DTAA) in force, which ensures that the same income is not taxed twice. Tax paid in India on income can be credited against your Spanish tax liability, and vice versa, depending on the income type and which country has primary taxing rights under the treaty.

The DTAA covers employment income, business profits, dividends, interest, royalties, and capital gains. This means that if you are paying tax in India on rental income from an Indian property, you will not pay the full Spanish rate on that same income, the Indian tax paid is credited. Your Spanish tax advisor applies the relevant DTAA articles when preparing your Modelo 100.

In most cases, if you leave India for employment abroad and spend more than 182 days outside India in a financial year, you will qualify as a Non-Resident Indian (NRI) for tax purposes under the Income Tax Act 1961. This is a legal status change with real financial and compliance implications.

Your existing resident savings accounts should be redesignated as NRO (Non-Resident Ordinary) accounts in accordance with the Foreign Exchange Management Act 1999 (FEMA). You may also open NRE (Non-Resident External) accounts to hold foreign earnings in India in a fully repatriable, tax-free rupee account. It is important to inform your bank of your change in residential status soon after relocating.

Your other Indian financial assets can continue with certain restrictions. Existing PPF accounts can be maintained until maturity but cannot be extended or newly opened once you become an NRI. NPS accounts can continue with contributions, and withdrawals are permitted subject to applicable rules. Mutual funds can also be held as an NRI, although some fund houses impose restrictions depending on your country of residence.

For EPF, you may withdraw your balance after leaving Indian employment. However, if you withdraw before completing five years of continuous service, the amount may be subject to tax, so timing your withdrawal carefully is important.

Money remitted from India to Spain by resident individuals is governed by the Liberalised Remittance Scheme (LRS), which allows outward remittances of up to USD 250,000 per financial year for permitted purposes such as living expenses, education, and investments.

Once you become a Non-Resident Indian (NRI), LRS no longer applies to you. Instead, your remittances are governed by the Foreign Exchange Management Act 1999 (FEMA) provisions applicable to NRO and NRE accounts. Funds held in NRE accounts are freely repatriable, while transfers from NRO accounts are subject to limits and documentation requirements.

However, during your transition year, or if funds are being sent on your behalf by family members who remain resident in India, the LRS limit continues to apply and must be observed.

For transferring money between Spain and India, services like Wise are widely used for their transparency and competitive exchange rates. Regardless of the method used, ensure that all international transfers comply with applicable banking and tax reporting requirements in both India and Spain.